This article explains what is blockchain technology and how does it work, examining its core components and diverse applications across various sectors. Blockchain is transforming how we handle data, transactions, and trust in the digital age, providing a decentralized and secure platform for recording and verifying information with unparalleled transparency and traceability.

Understanding the Basics of Blockchain

To fully understand “what is blockchain technology and how does it work,” it’s essential to simplify the concept.

What is Blockchain in Simple Words?

In simple terms, blockchain is a digital ledger that records transactions across many computers in such a way that the registered transactions cannot be altered retroactively. This decentralization ensures that no single entity has control over the entire chain, significantly enhancing security and trust. Think of it like a shared spreadsheet where everyone has access, and once a row is filled out, it can’t be changed without consensus from the group. To delve deeper into blockchain technology and its unique attributes, you can explore various resources available online.

The Concept of a Distributed Ledger

Blockchain technology operates on the principle of a distributed ledger. Unlike traditional databases that are centralized and managed by a single entity, a blockchain ledger is spread across multiple nodes (computers). Each node maintains a copy of the entire blockchain, ensuring that all transactions are transparent and verifiable. This architecture enhances resilience against fraud and tampering.

How Blockchain Differs from Traditional Databases

Traditional databases can be manipulated by those who control them, posing risks of fraud and data breaches. In contrast, blockchain technology creates an immutable record of transactions. Once data is recorded, it is nearly impossible to change without altering every subsequent block, which requires the consensus of the majority of the network. This inherent security makes blockchain a robust alternative to conventional databases.

Blockchain Example

A straightforward blockchain example involves tracking tuna from the fishing vessel to the consumer. Provenance, a company utilizing blockchain technology, tracks tuna caught by fishermen in Indonesia. Each catch is registered on the blockchain, recording details like the fishing method, date, and location. As the tuna moves through the supply chain—from processing to packaging and distribution—each step is logged. This allows consumers to scan a QR code on the tuna packaging and see the entire journey of their fish, verifying its sustainability and origin. This transparency builds trust, combats illegal fishing, and empowers consumers to make informed choices.

Key Features and Benefits of Blockchain Technology

Understanding the key features of blockchain technology is essential to appreciate its value proposition in today’s digital landscape.

Decentralization

Decentralization is one of the hallmark features of blockchain technology. This characteristic enhances security and resilience by eliminating single points of failure. In a decentralized system, the data is spread across numerous nodes, making it much harder for hackers to compromise the entire network.

Immutability

Immutability is another crucial aspect of blockchain. Once a transaction is recorded on the blockchain, it cannot be altered or deleted. Each block contains a unique cryptographic hash of the previous block, ensuring that any attempt to change data will be easily detectable by the network. For example, in a land registry system built on a blockchain, the history of ownership is permanently recorded. This prevents fraudulent activities like double-selling or forging ownership documents. This feature builds trust among users, as they can be confident that the records are accurate and tamper-proof.

Transparency

Transparency is vital for accountability in any transaction. In a public blockchain, all transactions are visible to anyone with access to the network. This openness helps prevent fraud and ensures compliance with regulations, as all parties can audit transactions in real time. The visibility of transactions can also lead to improved supply chain management, where stakeholders can trace product origins and verify claims. For more insights into the purpose of blockchain technology, you can explore additional resources that elaborate on its benefits and challenges.

Security

Security in blockchain technology is achieved through advanced cryptographic techniques. Each transaction must be verified by consensus among nodes before it can be added to the blockchain. This multi-layered verification process greatly reduces the risk of fraud and unauthorized access. Additionally, the decentralized nature of blockchain means that even if one node is compromised, the rest of the network remains secure.

Efficiency

Blockchain technology streamlines processes by removing intermediaries. Transactions can be processed faster and at lower costs since they don’t require third-party verification. This efficiency is particularly beneficial in industries like finance and supply chain management, where time and cost savings can significantly impact overall operations.

Types of Blockchain Networks

Understanding the different types of blockchains is crucial for recognizing their varied applications. A key differentiator is whether a blockchain is permissioned or permissionless.

Public Blockchains

Public blockchains, such as Bitcoin and Ethereum, are open to anyone. They operate without restrictions, allowing anyone to join the network, validate transactions, and maintain the ledger. This openness fosters innovation and encourages widespread participation. However, they can be slower and face scalability challenges as user demand increases.

Private Blockchains

Private blockchains are restricted to specific users, often within an organization. These blockchains provide enhanced privacy and control over data, making them suitable for enterprises that require confidentiality in their transactions. Private blockchains can also improve efficiency by limiting the number of participants and transactions that need to be verified.

Consortium Blockchains

Consortium blockchains are governed by a group of organizations. They offer a middle ground between public and private blockchains, allowing multiple parties to collaborate while maintaining some level of privacy. This model is often used in industries where several stakeholders need to share information securely, such as banking or supply chain management.

Hybrid Blockchains

Hybrid blockchains combine elements of both public and private blockchains, providing flexibility in data access and control. This adaptability makes them suitable for various applications across different sectors, allowing organizations to leverage the benefits of both blockchain types.

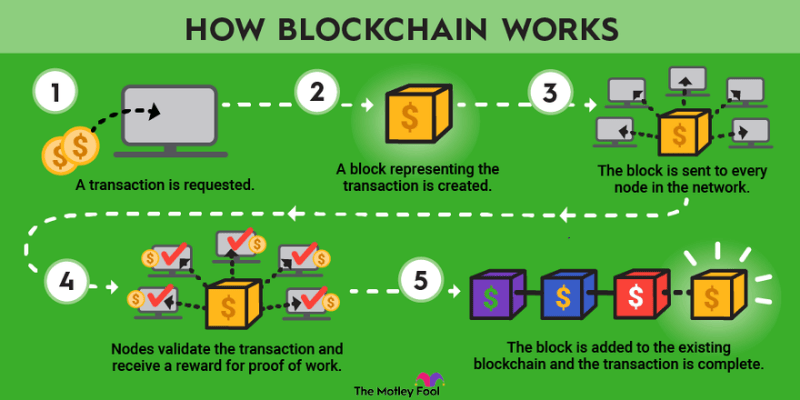

How Blockchain Works Step by Step

To truly understand “how blockchain works step by step,” let’s break down the process of a transaction from initiation to completion.

Transaction Initiation

The journey begins when a user initiates a transaction. This could involve sending cryptocurrency or executing a smart contract. Each transaction is encrypted using cryptographic keys—specifically, a public key (visible to everyone) and a private key (kept secret by the user).

Transaction Verification

Once a transaction is initiated, it is sent to the network of nodes for validation. Here, the nodes verify the transaction using consensus mechanisms. The two most common consensus methods are:

- Proof of Work (PoW): In this model, nodes (miners) compete to solve complex mathematical problems to validate transactions and create new blocks. The first miner to solve the problem gets to add the block to the blockchain and is rewarded with cryptocurrency.

- Proof of Stake (PoS): This method selects nodes to validate transactions based on the number of coins they hold and are willing to “stake” as collateral. PoS is considered more energy-efficient than PoW, reducing the overall environmental impact associated with blockchain transactions.

Block Creation and Addition

Once a transaction is verified, it is grouped with other verified transactions into a new block. Each block includes a timestamp and a unique cryptographic hash of the previous block, ensuring that the blocks are securely linked.

Transaction Completion and Immutability

After the new block is created, it is added to the existing blockchain, completing the transaction. The data within the block becomes immutable, meaning it cannot be altered without the consensus of the network. This process is what establishes the integrity of the blockchain.

Smart Contracts: Automating Business Processes

What are Smart Contracts?

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They run on blockchain technology, allowing for automated and secure execution without the need for intermediaries.

How Smart Contracts Work on a Blockchain

Smart contracts function by automatically executing actions when predetermined conditions are met. For example, in a supply chain scenario, a smart contract could automatically trigger payment to a supplier once goods are delivered and verified. This automation reduces delays and minimizes the potential for disputes, improving overall efficiency.

Real-World Examples of Smart Contract Applications

Smart contracts have numerous applications across various industries, including:

- Finance: Automating payment processes and ensuring compliance with regulatory requirements. Platforms like Compound and Aave utilize smart contracts to facilitate lending and borrowing.

- Supply Chain: Tracking goods and automating payments upon delivery. Smart contracts can trigger payments only when all conditions are satisfied, ensuring reliability and accountability.

- Real Estate: Streamlining property transactions by automating contract execution and title transfers, reducing the need for lengthy legal processes.

Blockchain Platforms and Enterprise Solutions

Several platforms facilitate the development and deployment of blockchain applications. Notable ones include:

Ethereum

Ethereum is a leading platform for creating decentralized applications (dApps) and smart contracts. It introduced Ether (ETH), its native cryptocurrency, which powers transactions and computations on the network. The flexibility of Ethereum allows developers to create a wide range of applications across industries.

Hyperledger Fabric

Hyperledger Fabric is designed for enterprise use, offering a permissioned blockchain framework suitable for private transactions and data sharing among organizations. It allows for customizable governance and confidentiality, making it an attractive option for businesses.

Other Platforms

Various other platforms, such as Corda and OpenChain, cater to specific needs, providing tailored solutions for different industries. Additionally, Coinbase serves as a prominent cryptocurrency exchange that allows businesses and individuals to buy, sell, and trade cryptocurrencies, making it relevant for organizations looking to integrate blockchain into their operations.

Blockchain Use Cases in Business

Blockchain technology has widespread applications across industries, enhancing efficiency and security.

Supply Chain Management

Blockchain enables real-time tracking of products, ensuring transparency and authenticity throughout the supply chain. This capability allows businesses to verify the origins of their products and enhance consumer trust. Companies like Walmart and Unilever are already leveraging blockchain to trace food products and ensure ethical sourcing.

Finance and Banking

In the financial sector, blockchain facilitates faster and more secure transactions. By reducing the need for intermediaries, blockchain can lower operational costs and mitigate fraud. For instance, Ripple uses blockchain technology to streamline cross-border payments, making them quicker and less expensive.

Healthcare

Blockchain can securely manage patient records, ensuring data privacy and interoperability among healthcare providers. This capability is crucial for maintaining patient confidentiality while enabling data sharing among authorized parties. Initiatives like MedRec are exploring how blockchain can improve health information exchange.

Other Industries

Blockchain has potential applications in real estate, voting systems, identity management, and more, showcasing its versatility and adaptability across various sectors. For example, blockchain can enhance the security and transparency of voting systems by providing a verifiable record of each vote cast.

Advantages and Disadvantages for Businesses

Advantages

- Enhanced Security: The decentralized nature and cryptographic techniques used in blockchain provide a high level of security against fraud and cyberattacks. However, blockchains are not immune to vulnerabilities. Smart contract bugs and 51% attacks (where a single entity controls the majority of the network’s computing power) are potential risks.

- Increased Transparency: All participants can access the same information, fostering trust and accountability. This transparency is particularly valuable in industries where traceability is crucial.

- Improved Efficiency: Transactions can be processed more quickly without intermediaries, reducing costs and saving time. This efficiency can lead to better resource allocation and overall productivity.

- Reduced Costs: By eliminating middlemen, blockchain can lower transaction fees and operational costs, making it an appealing option for businesses.

Disadvantages

- Scalability Challenges: As the number of users grows, the blockchain can become slower and less efficient, particularly in public blockchains. However, advancements like sharding and layer-2 solutions are actively being developed to address these limitations, and some blockchains, like Solana, are already achieving high transaction throughput.

- Regulatory Uncertainty: The lack of clear regulations in some jurisdictions can hinder the adoption of blockchain technologies. Organizations must navigate a complex legal landscape, which can be daunting.

- Complexity of Implementation: Integrating blockchain into existing systems can be complex and require significant investment. Businesses need to carefully consider the costs and benefits before making a transition.

The Future of Blockchain Technology

Emerging Trends

As we move forward, several trends are likely to shape the future of blockchain technology:

- Blockchain-as-a-Service (BaaS): Companies are increasingly offering blockchain solutions as a service, allowing businesses to integrate blockchain without the need for extensive infrastructure.

- Interoperability: Efforts to enable different blockchain networks to communicate with each other will likely enhance the overall effectiveness of blockchain applications.

- Zero-Knowledge Proofs (ZKPs): ZKPs allow one party to prove to another that a statement is true without revealing any information beyond the validity of the statement itself. This has significant implications for blockchain privacy and scalability, as it enables transactions to be verified without revealing sensitive data or requiring the entire network to process the details. This can significantly improve transaction speeds and reduce network congestion.

Potential Challenges

While blockchain holds great promise, several challenges remain:

- Scalability: Finding solutions to improve transaction speeds and network efficiency will be crucial for broader adoption. Current limitations stem from the need for every node to process every transaction. Solutions being explored include sharding (breaking the blockchain into smaller, manageable pieces), layer-2 scaling solutions (processing transactions off-chain), and new consensus mechanisms like Proof-of-Stake (PoS) which are less computationally intensive than Proof-of-Work (PoW).

- Regulatory Frameworks: Developing clear regulations will help foster innovation while ensuring consumer protection. Policymakers need to balance the desire for oversight with the need to encourage technological advancements.

- Energy Consumption: As concerns about the environmental impact of blockchain mining grow, alternative consensus mechanisms like PoS may gain traction. This shift could make blockchain more sustainable in the long run.

The Intersection of Blockchain and Cryptocurrency

Understanding the Relationship

Blockchain technology serves as the foundation for cryptocurrencies. While cryptocurrencies like Bitcoin and Ethereum operate on blockchain networks, blockchain itself is not limited to digital currencies. It can be used for a variety of applications beyond finance, including supply chain management, healthcare, and identity verification.

Decentralized Finance (DeFi)

Decentralized Finance (DeFi) refers to a range of financial services built on blockchain technology, allowing users to conduct transactions directly without intermediaries. This model provides greater access to financial services and can reduce costs. Examples of DeFi services include decentralized exchanges (DEXs) for trading cryptocurrencies, lending and borrowing platforms, and stablecoins pegged to fiat currencies.

Investing in Blockchain Technology

Investment Opportunities

Investing in blockchain can take various forms:

- Cryptocurrencies: Directly purchasing and holding cryptocurrencies like Bitcoin or Ethereum. This method allows investors to gain exposure to the growing cryptocurrency market.

- Blockchain Startups: Investing in emerging companies that are developing innovative blockchain solutions. These startups often offer unique technologies or services that could disrupt traditional industries.

- Blockchain Funds: Participating in investment funds focused on blockchain technology and related sectors. These funds provide a diversified approach to investing in blockchain without the need to pick individual assets.

Risks to Consider

Investing in blockchain and cryptocurrencies carries inherent risks, including market volatility, regulatory changes, and technological challenges. Conducting thorough research and considering risk tolerance is crucial for potential investors. It’s essential to stay informed about market trends and regulatory developments to make sound investment decisions.

Resources for Further Learning

For those interested in deepening their understanding of blockchain technology, various resources are available, including online courses, workshops, and educational PDFs. Additionally, platforms like Ethereum and Hyperledger offer extensive documentation to help developers get started. You can also find blockchain technology PDF resources and blockchain technology ppt presentations to facilitate learning.

Conclusion

Cryptomining technology offers significant potential for businesses seeking to enhance efficiency, security, and transparency. From streamlining supply chains to automating contracts with smart contract technology, blockchain’s applications are rapidly expanding. While challenges such as scalability and regulation remain, the transformative power of blockchain is undeniable. By understanding what blockchain technology is and how it works, businesses can position themselves for success in an increasingly digital world. Explore the resources available, such as online courses and blockchain technology PDFs, to delve deeper into this revolutionary technology and discover how it can benefit your organization.